DEMAND SLIDES FOR TENTH STRAIGHT QUARTER

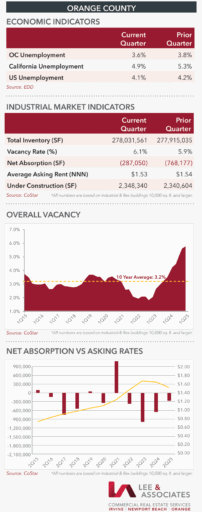

Overall demand for industrial space fell in Q2 for the tenth straight quarter, pushing up the vacancy rate to 6.1% from the 1.8% record low of late 2022. Increased vacancies translate into improved market conditions for tenants with rents falling more than 10% from their recent peak.

The reduced demand for industrial space reflects concerns about the impact of tariffs, which were blamed for declines in cargo through Los Angeles’ port complex. Year-over-year container traffic in May through the Port of Los Angeles was down 5% and off 8.2% at the Port of Long Beach.

Vacancy rate growth is serving to bring the industrial market more into balance. There is also a new surge in construction that will benefit large-space users. Developers are underway on 23 buildings, averaging 102,101 SF. This represents the greatest expansion since 2008, when 37 buildings were under construction, averaging 27,831 SF.

The overall vacancy rate at the end of the first half was 6.1%, the highest since 2012 when rents averaged $0.64 per SF, compared to the current average of $1.53 per SF triple net.

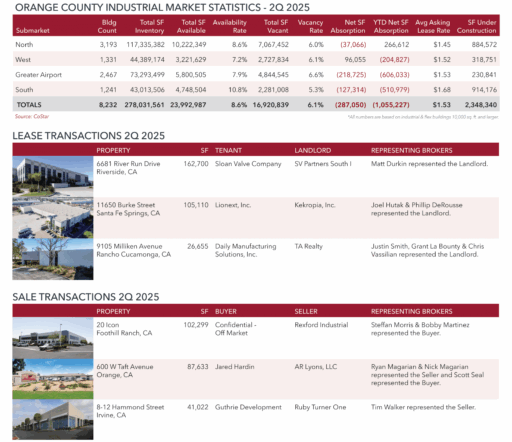

Countywide, there are 278 million SF of space in 8,232 buildings. Net absorption in the second quarter was negative 287,050 SF and was down across three of the county’s four submarkets. Although first-half demand was 1.1 million SF in the red, it was an improvement from the 2.7-million-SF contraction through Q2 a year ago.

The largest decline in net absorption was in the 73.3-million-SF Airport submarket, which posted a first-half drop of 606,033 SF. This was greater than the negative 578,271 SF for the first six months of 2024. The vacancy rate at the end of June was 6.6%, up from the 1.8% record low in early 2022. Net rents in Q2 fell to an average of $1.53 per SF, down from the $1.79 SF peak at the close of 2023. Three buildings totaling 230,842 SF are under construction.

West County, with 44,389 SF was the only submarket showing Q2 tenant growth. The 215,724 of net absorption reduced the vacancy rate 30 basis points to 6.1%, pushing up average rents slightly to $1.52 per SF. Three buildings are underway, totaling 318,751 SF.

In the 117.3-million-SF North County submarket, the vacancy rate ticked up slightly to 6% on 37,066 SF of negative net absorption. Two buildings totaling 236,218 SF were delivered in the second quarter. Six buildings are underway, totaling 884,572 SF.

In the 43-million-SF South County market, negative net absorption was 127,314 SF in Q1 and 510,479 SF year to date, driving up the vacancy rate to 5.3%. Eleven buildings are under construction, totaling 914,176 SF.

MARKET FORECAST

In Cal State Fullerton’s second-quarter survey of OC business leaders, the overall index improved to 68.6% from 52.2% in Q1. Thirty-eight percent of executives said they expected sales to increase in Q3 compared to 37% in the prior quarter. Inflation was replaced by interest rates, geopolitical risks and tariffs as the biggest concern.

ABOUT LEE & ASSOCIATES

Celebrating more than 46 years of leadership excellence in commercial real estate, Lee & Associates is the largest broker-owned firm in North America with locations across the U.S. and Canada.

With a broad array of regional, national and international clients – ranging from individual investors and small businesses to large corporations and institutions – Lee & Associates has successfully completed transactions with a total value of more than $32 billion in 2022.