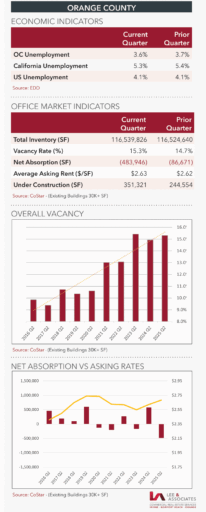

TREND OF IMPROVING DEMAND PAUSES IN SECOND QUARTER

Although there was a healthy level of leasing activity in the second quarter with about 23 full-floor transactions, overall demand for Orange County office space posted its biggest quarterly decline since late 2023. It ended the first positive trend for local landlords since the Covid lockdown. The overall vacancy rate increased 60 basis points in the second quarter to 15.3%, and Class A vacancy ticked up to 19.7%.

Whether the negative net absorption of 483,946 SF in the second quarter represents more than a pause will become clear in the coming quarters. But this latest reversal reaffirms market instability as tenants contract. There was a modest first-quarter drop of 86,671 SF, but Q2’s decline signals that the momentum behind the 1.48 million SF gained since late 2023 has lost steam.

Throughout 2024, Orange County had been one of the top performing markets in the United States. Fewer tenants had been relinquishing space upon lease expiration. Availability also declined due to more sublease space being leased, delisted, or expired. Second-hand space absorbed in 2024 totaled 437,065 SF, the most on record in a single year.

Development is at low ebb. There are only four projects totaling 351,321 SF under construction, down from a historical average of 1.8 million SF. Several planned projects have been mothballed due to weaker leasing prospects, and obsolete offices have been razed for redevelopment.

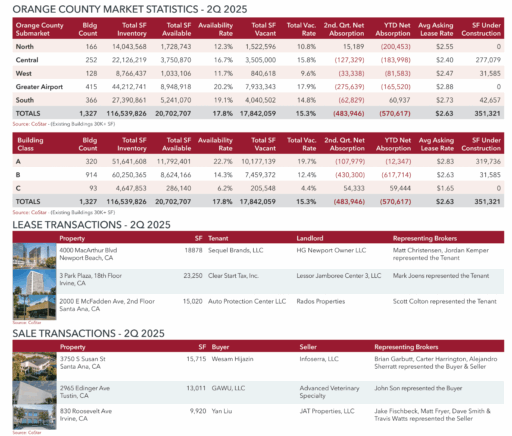

Year-to-date net absorption is in the red in four of the county’s five submarkets, whose inventory totals 116.5 million SF in 1,327 buildings. The Greater Airport is the largest, with 44.2 million SF and has the highest vacancy rate, 17.9%. There are 7.9 million SF of empty space throughout 415 buildings. The average asking lease rate is $2.88 per SF compared with the $2.63 per SF countywide average.

Among the county’s largest 2Q leases was the agreement for 62,977 SF in a 96,409-SF Class A tower at 5000 Birch St. in Newport Beach. The building was 80% vacant. The space had been available for six years.

The 8.8-million-SF West County market is the county’s smallest, with 128 buildings and tightest with a vacancy rate of 9.6%.

The 27.4-million-SF South County submarket, the county’s second largest, has a vacancy rate of 14.8% and is the only submarket posting positive first-half tenant growth totaling 60,937 SF.

The largest two sales in Q2 were the acquisition by H&S Ventures of Corona del Mar of the 262,000 SF Stadium Tower at 2400 E. Katella Ave., in Anaheim for $72.1 million or $275 per SF; and the 18-story City Plaza with 359,134 SF. It sold to Surlamer Investments of Newport Beach for $51.51 per SF. The property’s profile shows it at 22% occupancy.

MARKET FORECAST

In a new periodic survey by Cal State Fullerton’s business school, 38% of local business executives said they expect sales to increase, up from 37% in Q1. Thirty-eight percent said they would hire more workers, compared to 17% in the first quarter. Interest rates, geopolitical risks, and tariffs have displaced inflation as their leading concern.

ABOUT LEE & ASSOCIATES

Celebrating more than 46 years of leadership excellence in commercial real estate, Lee & Associates is the largest broker-owned firm in North America with locations across the U.S. and Canada.

With a broad array of regional, national, and international clients – ranging from individual investors and small businesses to large corporations and institutions – Lee & Associates has successfully completed transactions with a total value of more than $32 billion in 2022.