STRONG TENANT DEMAND RETURNS IN THIRD QUARTER

Demand for office space returned in the third quarter with one of the strongest three-month periods of net absorption since the 2020 Covid lockdown.

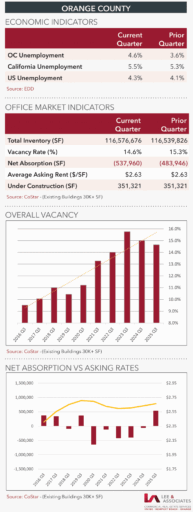

Tenant demand increased across four of the county’s five submarkets in the third quarter with net absorption totaling 537,960 SF, reversing most of the recent weakness.

Despite its muted office-using payroll growth, Orange County office space continues to outperform many of its urban peers. Since 2023 there have been 1,432,179 SF of net absorption and vacancy has fallen from a record 15.7% to 14.6% in the last two years while, nationally, vacancy has been on the rise.

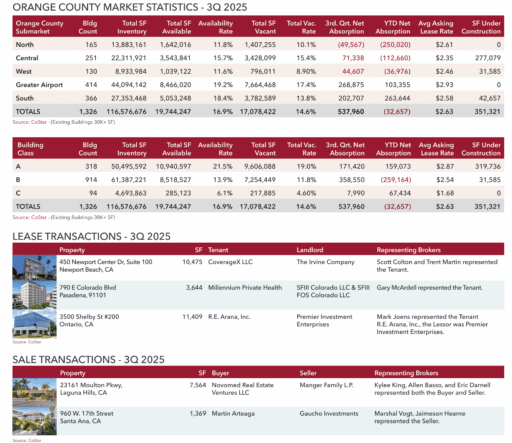

There are 116.6 million SF in 1,326 buildings at least 30,000 SF in Lee & Associates’ quarterly survey. The volume of premium space totals 50.5 million SF, or 43% of the total inventory. There are 61.4 million SF of Class B space.

In addition to flat office-using employment, obsolete buildings are giving way to demolition and redevelopment generally for industrial use. Additionally, net leasable space has been reduced by 3 million SF from property purchased by owner-users since 2020.

Although most of the empty space is in the 318 Class A buildings, demand for premium space has been healthier recently. There were 171,420 SF leased in Q3 and 159,073 SF leased year to date, driving down the Class-A vacancy rate to 19% and reducing the availability rate by 220 basis points to 21.5%, a market-leading high.

Rents for premium space are inching downward overall, and landlords continue to offer aggressive concessions. Businesses are slowly moving back into high-rise towers, but many tenants have favored the easier access offered in low-rise, campus-style buildings with adjacent parking.

There was 358,550 SF of third-quarter tenant expansion in Class B properties, which total 61.4 million SF in 914 buildings countywide. The largest office lease of the third quarter and for the year was Hyundai’s 67-month agreement for 134,000 SF at 2300 Main Street in Irvine. Foundation Building Materials leased a 48,972-SF building at 2510-2520 Red Hill Ave. in Santa Ana.

The largest sale of the third quarter was Cress Capital LLC’s $41-million purchase of 1301 Dove Street in Newport Beach for $41 million or $190.79 per SF. The seller of the Class-A, 214,898-SF, 10-story tower was Western Alliance Bank of Phoenix. The building last sold for $298 per SF in 2021.

Platinum Triangle Partners LLC purchased the 123,5677-SF building at 2099 S. State College Blvd., Anaheim, for $19.7 million or $159.41 per SF. The Class-A building previously sold for $233 per SF in 2018.

MARKET FORECAST

About 22% of local business executives surveyed by Cal State Fullerton said they expect to increase their labor force in Q4 compared to 18% in Q3. Nine percent expect to cut jobs compared to 14% in Q3. Unease over interest rates overshadowed inflation as the most common concern

ABOUT LEE & ASSOCIATES

Celebrating more than 46 years of leadership excellence in commercial real estate, Lee & Associates is the largest broker-owned firm in North America with locations across the U.S. and Canada.

>With a broad array of regional, national and international clients – ranging from individual investors and small businesses to large corporations and institutions – Lee & Associates has successfully completed transactions with a total value of more than $32 billion in 2022.