2022 Q2 Economic Reports

GDP GROWTH: TRENDING IN Q2 2022

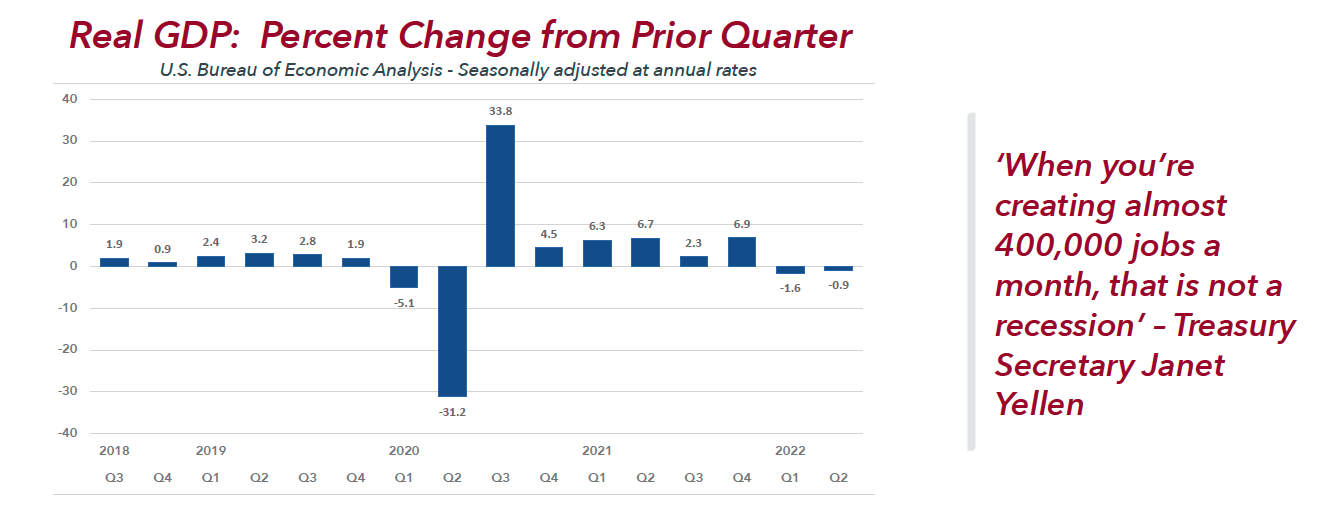

The U.S. economy contracted for the second straight quarter as a tightened monetary policy and high inflation took more steam out of consumer spending and businesses trimmed inventories.

The Commerce Department said the nation’s gross domestic product – the value of all goods and services sold – fell by an 0.9% annualized rate in the second quarter. The new reading coupled with the 1.6% first-quarter decrease means the economy has met the common definition for recession.

But top officials in the Biden administration and Federal Reserve say the recession label doesn’t apply because job growth, industrial production, spending and incomes all remain robust. The unemployment rate has been steady at a low 3.6% for the last two quarters. Employers have hired for 1.56 million positions over four months ending in June. Unemployment claims were at a 52-year low.

“A recession is broad-based weakness in the economy. We’re not seeing that now,” said Treasury Secretary Janet Yellen. “When you’re creating almost 400,000 jobs a month, that is not a recession.” U.S. employers hired more workers than expected in June, and wages gained 5.1% year over year. A new report showing the personal consumption expenditures index dropping to 4.4% was another bright spot.

Nevertheless, there were growing indications of cooling in the job market, with new claims for jobless benefits, for instance, edging up in late in the second quarter. Personal consumption data showed spending and disposable income dropped on an inflation-adjusted basis. Consumer spending, which makes up about two-thirds of total economic output, rose at a 1% annual rate in Q2, down from 1.8% in the first quarter. “It’s the pieces of the puzzle that matter when you’re looking at GDP,” said Michelle Meyer, U.S. chief economist at the Mastercard Economics Institute. “I think a lot of it comes down to jobs,” she said. “Whether you have a job. Whether you expect to keep your job.”

The consensus view among analysts is: if the economy is in a recession, it’s a mild one. If not, a recession virtually is certain later this year or in 2023. But the immediate concern is high inflation, which is seen by central bankers and other policymakers as the most insidious of economic ailments.

Federal Reserve Chairman Jerome Powell has declared that shutting down high inflation, even at the risk of tipping the economy into recession, is the priority. After raising the benchmark rate three-quarters of a point in late July, Powell said that slower growth in consumer spending, weakening housing demand and lower business investment are signs the Fed’s strategy is working.

“Our goal is to bring inflation down and have a so-called soft landing, by which I mean a landing that doesn’t require a significant increase in unemployment. We understand that’s going to be quite challenging. It’s gotten more challenging in recent months,” he said.

EMPLOYMENT: TRENDING IN Q2 2022

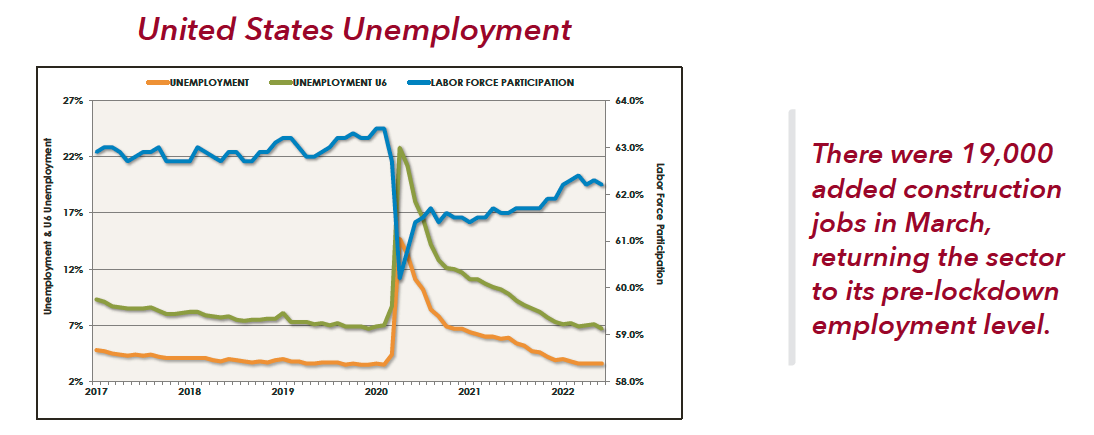

Payrolls increased by 372,000 jobs in June, more than expected. The unemployment rate was 3.6% for the fourth straight month while the number of jobless essentially was unchanged at 5.9 million. It was another strong showing for the job market. Although it may not ease worries of a recession, economists believe the strong employment data improves the chances for a soft landing.

The Labor Department also reported that average hourly earnings increased 0.3% and were up 5.1% from a year ago. The strong wage growth enables the Federal Reserve to press ahead with planned increases in interest rates, while watchful of the effects that wage growth could have on rising costs.

“Wages are not principally responsible for the inflation we’re seeing, but going forward they would be very important, particularly in the service sector,” said Fed Chairman Jerome Powell at his news conference in June. The report was better than the Dow Jones estimate of 250,000 jobs, continuing what has been a healthy year for job growth. It follows gains of 384,000 in May and 368,000 in April and 431,000 in March.

Moreover, the current job totals broadly are close to the 3.5% unemployment rate and 5.7 million jobless reported in February of 2020, prior to the lockdown. Nevertheless, private-sector payrolls exceeded pre-pandemic totals in June with restoration of the 21 million jobs that were lost following the lockdown.

Not all jobs were in the same industries. There are more e-commerce and white-collar jobs than before the pandemic but restaurant and government employment are lagging. Warehousing and transportation have grown the fastest, a Labor Department analysis said. Employment in white-collar jobs, such as professional and technical services, technology-heavy information and finance, all was greater than in February of 2020.

Industries that make, sell and deliver goods, including manufacturing, construction and retail, fully recovered lost jobs. But government employment remains depressed as public schools, hospitals and transit systems slowly recover their staffs. Leisure and hospitality also has a large gap to close.

In June, education and health services jobs were the leading growth categories with 96,000 hires. Professional and business services added 74,000 positions. Leisure and hospitality added 67,000 jobs. There were 57,000 health-care jobs and 36,000 new positions in transportation and warehousing. Manufacturing added 29,000 jobs. Information and social assistance jobs gained 25,000 and 21,000 respectively. Government jobs fell by 9,000.

Job openings continue to be robust after setting records and the shortage of workers for office jobs is acute. A Conference Board survey in March reported that 84% of employers hiring professional office workers found it difficult to find talent. That was up from 60% the previous April.

Retail jobs in home-goods and big-box stores were able to fill positions beginning early in the lockdown. But retail employment has fallen since February as more Americans have been spending on travel. Driven single-handedly by the residential sector, construction jobs fully recovered in the spring. Commercial construction has been slower to recover since initial cutbacks in February 2020.

MONETARY POLICY: TRENDING IN Q2 2022

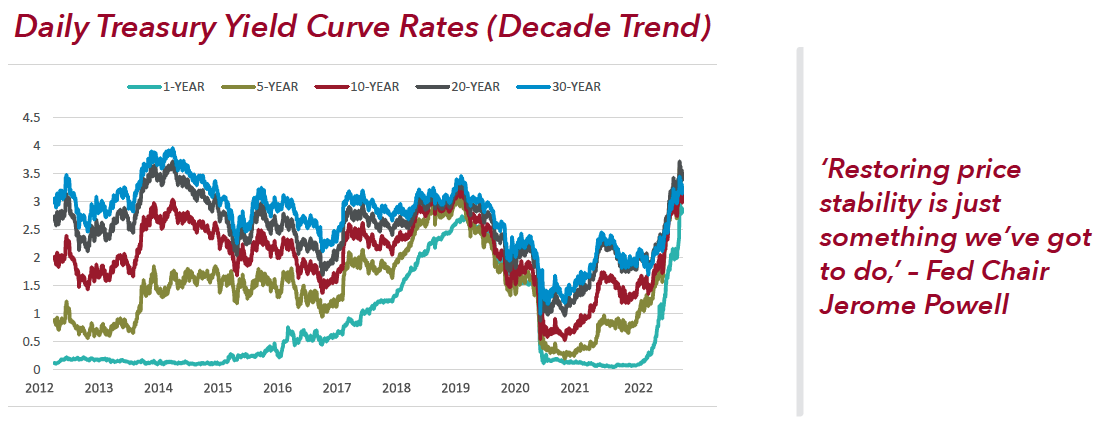

Federal Reserve officials affirmed the institution’s commitment to reducing the rate of inflation even if it heightens the risk of putting a slowing U.S. economy into a recession. Toward that goal the central bank’s Federal Open Market Committee in late July unanimously voted to raise the benchmark interest rate by three quarters of a percentage point. Short-term borrowing rates now are between 2.25% and 2.50%. The increase was expected and welcomed by the markets. It was on the heels of a 75-basis point rate hike in June, the largest single jump since 1994. It was the fourth rate hike this year. The increases were viewed by policymakers as necessary to control the cost-of-living increases, which were running at their highest levels since 1981.

Even before the latest rate hike, attention was being focused on the central bank’s next meeting in September and any clues Fed Chair Jerome Powell may offer on what to expect in the second half. In his announcement, Powell left no doubt about the Fed’s resolve, saying another “unusually large” hike may be needed in September if price pressures have not sufficiently cooled.

“Restoring price stability is just something we’ve got to do,” Powell said. “There isn’t an option to fail to do that.” The central bank’s own projections from June estimate that the Fed will need to rase rates to about 3.8% next year to bring inflation under control.

Powell disputes the claim that the U.S. is in a recession. That the traditional definition – two straight quarters of declining growth – includes high unemployment. But the current jobless rate is 3.6%, and weekly claims are at a 52-year low. One of the major criticisms of Powell is that the central bank lost control of inflation by abandoning its decades-long strategy of pre-emptive restraint – in other words, tightening the money supply before inflation takes hold.

Critics say the error was committed in August 2020. That’s when policymakers announced that rates would remain low “until labor market conditions reached levels consistent with the committee’s assessments of maximum employment and inflation has risen to 2% and is on track to moderately exceed 2% for some time.”

The new attitude encouraged the central bank to label the emerging inflation threat as “transitory.” In June of 2021, Powell said: “We will not raise interest rates pre-emptively because we think employment is too high, because we fear the possible onset of inflation. Instead, we will wait for actual evidence of actual inflation of other imbalances.”

Because of economic shocks stemming from Russia’s invasion of Ukraine and price pressures for food and energy, inflation exploded from 2% in December 2021 to 9.1% in June 2022. Along with the latest increase, the Fed announced: “In assessing the appropriate stance of monetary policy the committee will continue to monitor the implication of incoming information for the economic outlook. The committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the committee’s goals.”

GLOBAL ECONOMY: TRENDING IN Q2 2022

There is no shortage of pessimism in the outlook as the global economy increasingly appears headed for a recession. Russia’s invasion of Ukraine continues with no peaceful end in sight and the humanitarian crisis triggered by the war is widening. Trading disruptions of food and commodities since the invasion are driving up costs, adding to global inflation and increasing stress on vulnerable nations with large populations in extreme poverty. Businesses across the eurozone report continuing inflation pressures and an acceleration in wage growth.

Inflation in the currency union was growing at 8.6% in June, a reading that was followed immediately with a half-point increase in interest rates by the European Central Bank. It was the first rate hike in 11 years and greater than expected from the ECB, the central bank for 19 countries.

In June, Russia halted shipments of natural gas through Gasprom’s Nord Stream 1 pipeline, ostensibly for a month of repairs and not as punishment for Germany’s support for Ukraine or a wedge between European nations supporting sanctions, as widely believed. The pipeline was reopened in mid-July but the shutdown cut gas to Germany by 60% and reduced shipments elsewhere in Europe. Now threatened with recession and fearing Russia may cut vital gas shipments again, Germany has been racing to stockpile natural gas for winter.

Russia’s move has raised urgency of fuel supplies throughout Europe. There are 28 liquid natural gas terminals in Europe but none in Germany. There are four terminals in France, three in Italy and one in Belgium, Holland, Poland, Portugal, Spain, Lithuania, Greece and Malta. Many nations also are increasing gas storage capacities and loosening restrictions on coal.

Russia’s move has raised urgency of fuel supplies throughout Europe. There are 28 liquid natural gas terminals in Europe but none in Germany. There are four terminals in France, three in Italy and one in Belgium, Holland, Poland, Portugal, Spain, Lithuania, Greece and Malta. Many nations also are increasing gas storage capacities and loosening restrictions on coal.

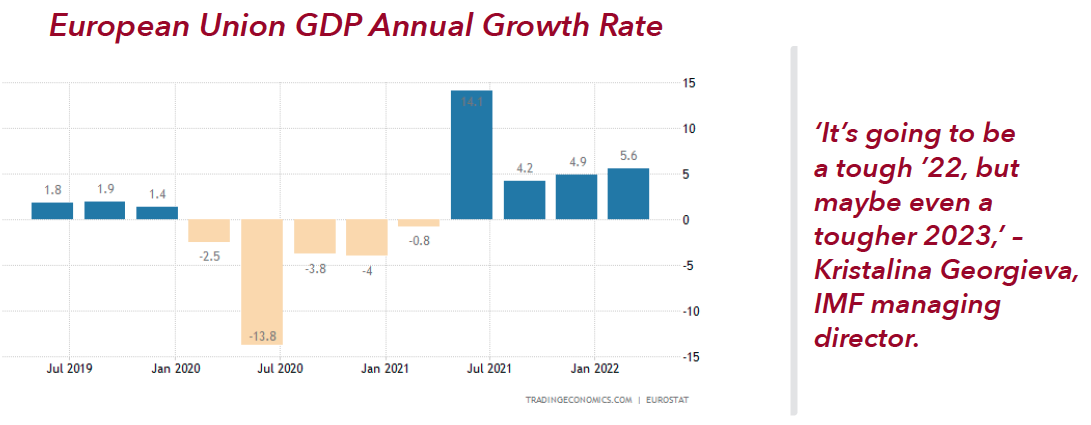

Kristalina Georgieva, managing director of the International Monetary Fund, said at the start of the third quarter that the global economy had “darkened significantly” since spring. She said the IMF would downgrade its 2022 forecast at 3.6% in the coming weeks for the third time this year. “

We’re in very choppy waters,” she told Reuters, and would not rule out a global recession. She said some large economies had contracted in the second quarter, including China, and that the risks were increasing. “It’s going to be a tough ’22, but maybe even a tougher 2023,” she said. At the close of the second quarter a number of analysts also were downgrading earlier forecasts and predicting a recession before the end of the year.

Adding to the global stress is the muscular U.S. dollar. The greenback has been surging for the last year against major global currencies, widening trading differences not seen in two decades. The dollar has gained 15% against the British pound, 16% against the euro and 23% against the yen, as Japan’s government recently cut its forecast for domestic growth.

“The preliminary purchasing managers index data for July point to a worrying deterioration in the economy,” said Chris Williamson, S&P Global’s chief business economist.

The information and details contained herein have been obtained from third-party sources believed to be reliable, however, Lee & Associates has not independently verified its accuracy. Lee & Associates makes no representations, guarantees, or express or implied warranties of any kind regarding the accuracy or completeness of the information and details provided herein, including but not limited to, the implied warranty of suitability and fitness for a particular purpose. Interested parties should perform their own due diligence regarding the accuracy of the information. The information provided herein, including any sale or lease terms, is being provided subject to errors, omissions, changes of price or conditions, prior sale or lease, and withdrawal without notice. Third-party data sources: CoStar Group, Inc., The Economist, U.S. Bureau of Economic Analysis, U.S. Bureau of Labor Statistics, Congressional Budget Office, European Central Bank, GlobeSt.com, CoStar Property and Lee Proprietary Data.

© Copyright 2022 Lee & Associates all rights reserved. Third-party Image sources: sorbis/shutterstock.com, shutterstock.com, pixabay.com, istock.com