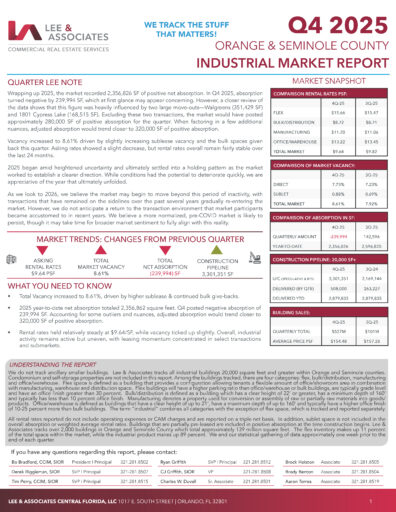

The Central Florida industrial market closed 2025 in a stronger position than 2024. The market has entered a period of “normalization” following several years of elevated activity after COVID, followed by a down 2024 year.

by a down 2024 year.

At the end of 2025, the market recorded 2,356,826 square feet of positive net absorption, despite negative absorption (239,994 SF) in Q4 that was driven primarily by a small number of large tenant move-outs rather than broad-based weakness. On a positive note, 2025 annual absorption was up 56% over 2024, and on par with 2023’s absorption numbers.

Vacancy ended the year at 8.61%, reflecting a market that is still quite healthy and not overbuilt. New construction deliveries declined by 17.5% from 2024 to 2025, with approximately 2.9 million square feet delivered in 2025 compared to nearly 3.5 million square feet in 2024. New supply slowed in 2025 with deliveries still outpacing net absorption. Looking ahead, the construction pipeline has increased to 3.3 million square feet slated to deliver in 2026. We view this as positive sign that developers are starting to bet on the market again.