The COVID-19 Real Estate Discount: Fact or Fiction

July 2021 – The COVID-19 Real Estate Discount: Fact or Fiction

Robert Leveen, Senior VP

As published in Receivership News, Summer 2021, Issue 72, Robert Leveen, Senior Vice President at Lee & Associates – Pasadena discusses the COVID-19 Real Estate Discount: Fact of Fiction.

**********

A few times a month, I receive a call from an appraiser to confirm pricing on a recently closed transaction. Once I report the numbers, invariably I get the question, “What do you think is the COVID-19 discount?” It is the question of the day. However, there is no simple response. Each commercial real estate product type has been subject to different economic forces which have played out during the pandemic. The following breaks it down by the four main product types, with our focus on the Los Angeles Metropolitan Statistical Area (MSA):

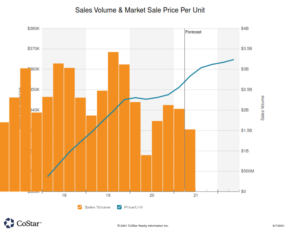

| Multifamily: The apartment building transactions I closed in the last twelve months, all in city of Los Angeles, had at the most a 3% discount to 2019. One of the properties had 25% vacancy as the seller never attempted to lease the units after tenants had vacated in the year prior. Early in the pandemic, lending locked up, but only for a short time. Then, lenders slowly returned to financing acquisitions, along with requiring increased reserves. And with lower interest rates, the sector has been largely shielded from significant value adjustment. As one can see by the chart, values continue to push higher. Overall, physical vacancy rate is up in the MSA. Additionally, economic vacancy has increased. This is when a tenant is delinquent, or has stopped paying altogether, totaling 5.8%, a significant jump from 4% over the trailing three years. In higher demand locations such as West Los Angeles and Santa Monica, asking rents declined by 10-15% from 2019. As of this writing in early June, the state eviction moratorium is set to expire June 30. If not extended, it will kick off a tsunami of unlawful detainer filings, forcing many tenants to relocate. Most landlords will digest the unpaid rent and move on. New multi-family developments (24,000 units currently under construction) which will be delivered in the next 12 to 18 months, will add new supply. Even so, thanks to the success of the vaccine, it is now anticipated positive rent growth will return to the MSA much faster than predicted just six months ago. |  |

|

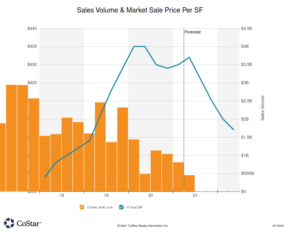

| Office: As many of us are working from home, office buildings have not seen this pace of occupancy erosion since 2008-2009. Market vacancy is at 13.5%. However, what is a perfect example of the tail wagging the dog is a tremendous increase of available sublease space to the tune of 9.5 million square feet. By comparison, there was 468,000 SF of sublease space available at the end of Q1, 2020. This could negatively impact valuations, if the tenants look to landlords for rent relief or initiate renegotiation. There was little to no effect on pricing in 2020, but MSA sales volume dipped by 45% compared to 2019, from $7.7 billion to $4.2 billion, indicating investors pushed the pause button. There are two competing schools of thought. One is office tenants will shed space as working remotely continues to be in favor. Conversely, in the long run, demand for space may increase as tenants seek to spread workers out. |  |

|

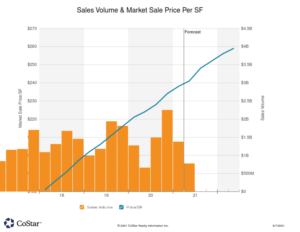

| Industrial: Even with the juggernauts of the ports of Los Angeles and Long Beach driving the industrial market for decades, new development is challenging due to high land cost, and a lack of large sites in the MSA. Most of the inventory is older and smaller. But the demand for logistics still exists. The increased demand for industrial and warehouse space has become even more pronounced in the pandemic. Amazon continues its real estate acquisition spree, recently closing on the old Orange County Register property in Santa Ana. As part of their last mile distribution network, it will redevelop it into a 110,000 SF fulfillment center for Orange County. Average sold price per square foot increased from $218 to $234, or 7.34%, over the end of 2019. Average Cap rates compressed to 4.6%. The market vacancy has declined to 2.5% from a pandemic high of 3.2%, further supporting forecasts of continued upward movement with deals trading in the $250 per square foot range in the latter part of 2021. |  |

|

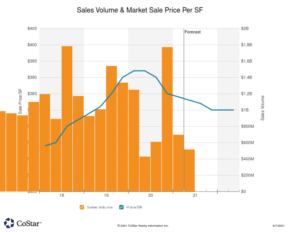

| Retail: This sector was already seeing softening prior to the pandemic driven by Internet-based sales. The challenges will continue and, consequently, values will adjust. On a personal experience level, I have a DTLA retail listing which went under contract just prior to the pandemic at $32,000,000, with $1.7 million of annual in-place income, and the buyer’s intention was to redevelop into multi-family. The pandemic caused the transaction to fall apart. As of this writing, we are now at the court confirmation and overbid stage with the first overbid increment set at $23,000,000. This particular property suffered two-fold. One, from loss of in-place income due to lockdowns. And two, valuations for infill developable land have declined. Along with notable inflation on lumber and steel, construction costs have risen significantly, adding more risk to an already risky venture. Similarly, vacancies have increased from 4.8% to 5.5% over the trailing fifteen months. Average sold price per square foot declined from $392 to $383. While only a 2.3% decline, it is anticipated the decline trend will continue in the near term before stabilizing. Our office is forecasting small retail strip centers with mom-and-pop tenants will continue to struggle well beyond 2021. For property owners with significant debt, and lenders unwilling to offer forbearance, it will leave them with few options. |  |