Since 1921, section 1031 exchanges have been an important part of the tax code. They have served as a vital and dependable stimulant not only to the real estate market but to the broader economy, yet nearly every election cycle there are always attempts to repeal them or restrict their use either through legislative actions or agency rule changes. These attempts stem from, among other things, suspicious attitudes about tax incentives for capital holders, negative press about “real estate moguls” and “big corporation”, and the widespread misunderstanding of key tax concepts such as reinvestment of capital, like kind, basis, deferral, and depreciation. This report will explain the benefits of 1031 exchanges and how they positively affect both real estate markets and the larger economy as a whole.

What is a 1031 Tax Deferred Exchange:

The 1031 Exchange allows you to sell one or more appreciated assets (generally rental or investment real estate, but could be non-real-estate) and defer the payment of your capital gain taxes by acquiring one or more replacement properties (many other complexities such as debt replacement, rigorous time frames and “like kind” concepts are also present).

-

1031 exchanges encourage investment and reinvestment in U.S. assets and make it easier for taxpayers to relocate or upgrade into assets that better meet their business needs.

-

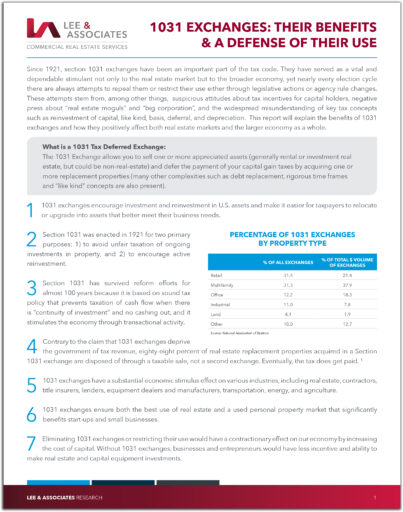

Section 1031 was enacted in 1921 for two primary purposes: 1) to avoid unfair taxation of ongoing investments in property, and 2) to encourage active reinvestment.

-

Section 1031 has survived reform efforts for almost 100 years because it is based on sound tax policy that prevents taxation of cash flow when there is “continuity of investment” and no cashing out, and it stimulates the economy through transactional activity.

-

Contrary to the claim that 1031 exchanges deprive the government of tax revenue, eighty-eight percent of real estate replacement properties acquired in a Section 1031 exchange are disposed of through a taxable sale, not a second exchange. Eventually, the tax does get paid. 1

-

1031 exchanges have a substantial economic stimulus effect on various industries, including real estate, contractors, title insurers, lenders, equipment dealers and manufacturers, transportation, energy, and agriculture.

-

1031 exchanges ensure both the best use of real estate and a used personal property market that significantly benefits start-ups and small businesses.

-

Eliminating 1031 exchanges or restricting their use would have a contractionary effect on our economy by increasing the cost of capital. Without 1031 exchanges, businesses and entrepreneurs would have less incentive and ability to make real estate and capital equipment investments.

-

The forced immediate recognition of gain upon the disposition of investment real estate and other capital assets will result in a higher cost of capital, greater reliance on debt financing, and will serve as a deterrent to investment in new assets.

-

Requiring the recognition of gain on Section 1031 exchanges would hamper businesses’ ability to be competitive in our global marketplace. Read More >