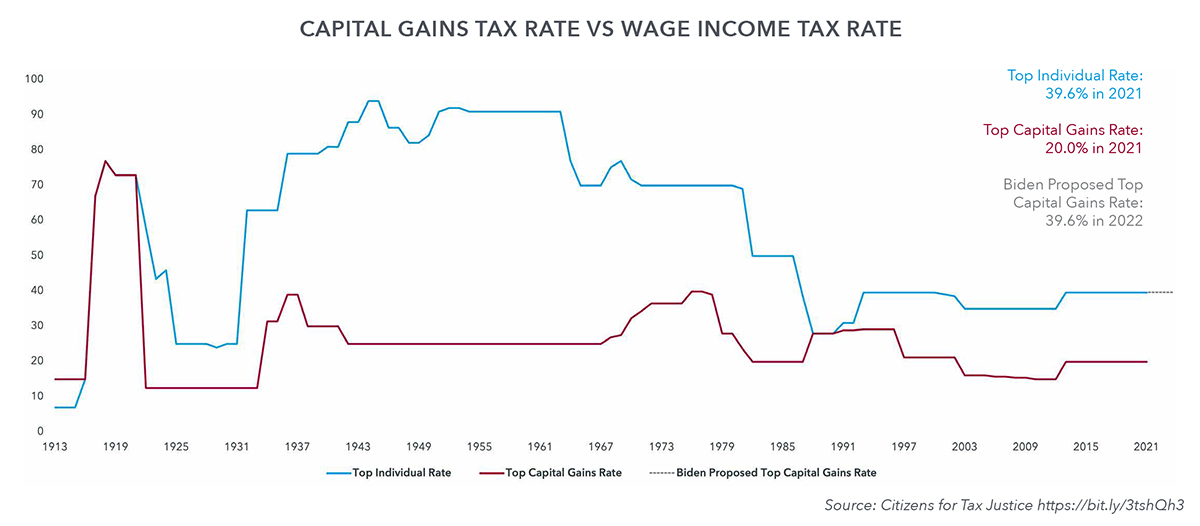

Currently, the top tax rate on capital gains, which applies to higher-income earners, is 20%. President Biden would increase the capital gains rate for those with incomes of over $1 million per year to the top rate on ordinary income, which under his plan would increase to 39.6%. If you include the current 3.8% net investment income tax that is imposed on those earning more than $200,000 annually ($250,000 for married couples), then the increase would be from 23.8% to 43.4%, an almost doubling of the capital gains tax rate for high-income investors.

For historical perspective, when the modern income tax was created in 1913, capital gains were taxed at the same rates as ordinary income — as high as 77% in 1918--the year World War I ended.

After the war, Congress lowered the top individual tax rate to 58% in 1922 and split off capital gains from regular income, slashing the rate to 12.5%.

Since then, capital gains rates have been changed frequently, climbing as high as 40% but typically remaining much lower than the top rate on ordinary income. The capital-gain-tax rate is currently 20% on incomes over $441,450 and 15% on incomes from $40,001 to $441,450. There is no capital gains tax on income of $40,000 or less.1

The top marginal tax rate on capital gains has historically been much lower than that for ordinary income, although the gap has narrowed as overall tax rates have come down. The Biden administration’s proposal would eliminate the gap entirely.2