REITS VS REAL ESTATE INVESTMENT FUNDS

Often confused with real estate investment funds, a REIT (real estate investment trust) is a corporation, trust, or association that invests directly in actual income-generating real estate assets such as industrial buildings, office parks, data centers, self-storage, hotels, or apartments and is traded like a stock. (A good example of a REIT to keep in mind is Prologis.) A real estate fund, by contrast, is a type of mutual fund that specializes in investing in stocks or bonds offered by public real estate companies, including REITs. (The classic example of a real estate investment fund is Vanguard’s Real Estate ETF.) Although either can be used to diversify your investment portfolio, there are essential differences between these two types of investment vehicles.

There are three types of REITs: Equity REITs, Mortgage REITs, and Hybrid or Combo REITs. Equity REITs own and operate income-producing real estate. In contrast, Mortgage REITs lend money to real estate owners and operators either directly through mortgages and loans, or indirectly by acquiring mortgage-backed securities. The majority of revenue associated with equity REITs comes from real estate property rent, while the revenue associated with mortgage REITs is generated from the interest earned on mortgage loans.

Because real estate funds are like other mutual funds, they can be managed either actively or passively. Those that are passively managed typically try to mimic the performance of a benchmark index. For example, the Vanguard Real Estate ETF (VNQ), which invests in REITs that buy office buildings, hotels, and other properties, tracks the MSCI US Investable Market Real Estate 25/50 Index.[1] Moreover, real estate funds invest primarily in REITs and real estate operating companies; however, some real estate funds invest directly in properties. Real estate funds gain value mostly through appreciation and generally do not provide short-term income to investors the same way that REITs do via dividends.[2]

This report will highlight how REITs have been performing since the onset of the pandemic, especially with regard to property rent as this is the primary source of revenue for most REITs, and will explain what their performance tells us about the economy and what to expect from them for the rest of 2020.

HIGHLIGHTS OF HOW REITS HAVE PERFORMED SINCE COVID-19

- The early weeks of the stay-at-home orders and business shutdowns were accompanied by steep declines of share prices across all REIT sectors. The FTSE All Equity REITs index had a total return of negative 7.0% in February, slightly less than the minus 8.2% total return on both the Russell 1000 and the S&P 500. Lodging and resorts, which bore the initial brunt of the shutdown in travel, posted a negative 13.9% total return in February.

- Even during the early stages of the pandemic, not all of the effects of the crisis were negative. Data centers and infrastructure REITs have often risen during the COVID-19 crisis, as use of online communications and cell phone traffic boosts demand for the servers that house the internet and for the cell towers that transmit voice and data communications. Data centers posted a total return of 10.5% in March, while infrastructure was little changed.

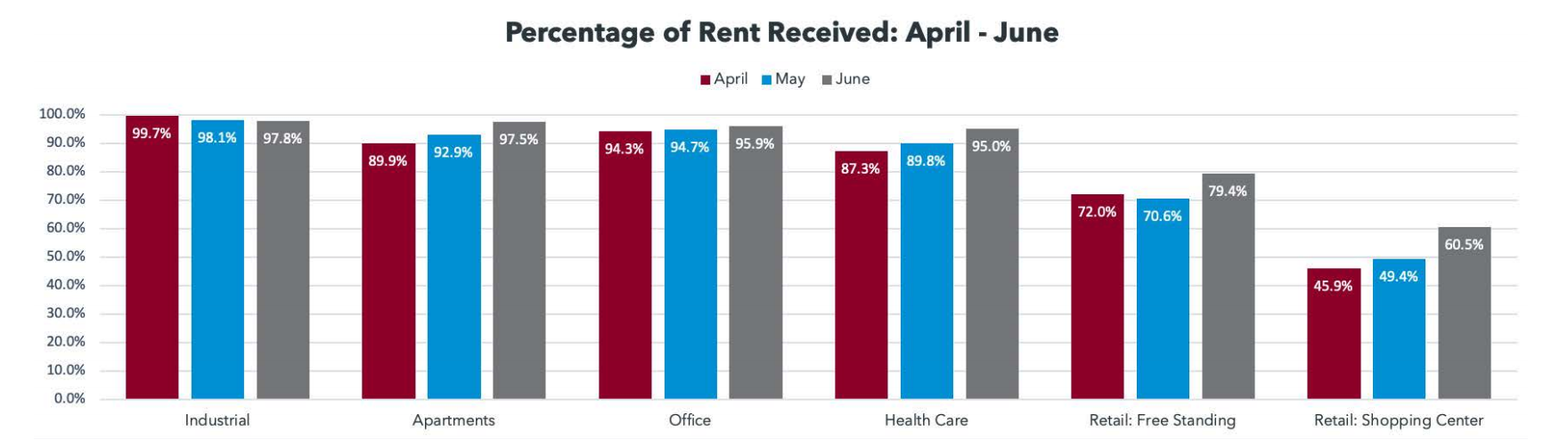

- NAREIT’s latest June survey of its members indicates an improvement for most sectors compared with May with large improvements in the retail subsectors for free standing and shopping center-focused REITs, suggesting that re-openings of the retail sector in many parts of the country in May have had a positive economic impact for retail REITs.

- Moreover, the industrial sector remained the strongest performer with collections equal to nearly 98% of typical rents in June, however industrial REITs show a slight downward trend from April to June. Survey respondents in May and June did not report any forbearance but did report deferrals of less than 1% of sector rent in both months. Industrial REITs own nearly 4,900 industrial properties in the U.S.

- The office sector’s June rent collections experienced a slight increase to 96% from 95% in May. By equity market cap, 82% of office REITs in the sample received more or the same share of rent collected in June than May. June survey respondents reported deferring 1.4% of sector rent owed by equity market cap. There are nearly 1,800 REIT-owned office properties in the U.S..

- In the retail sector, there are more than 16,000 REIT-owned free standing retail establishments across the U.S., including big box stores, pharmacies, convenience stores and restaurants. June results for free standing showed a rebound from May’s slightly lower number, with 79% of typical rents paid, up from 71% in May. May and June survey respondents in free standing reported granting rent deferrals for 17% of their May and June rent respectively.

- The U.S. has nearly 2,700 REIT-owned shopping centers. Shopping center REITs saw the biggest increase in rent collected with an 11 percentage point gain in June over May to nearly 61% of typical rent collected. This reflects an increase in rent collected for 67% of shopping center REITs by equity market cap. The sector’s deferral and forbearance rates for June survey respondents show REITs granting deferrals for 9% of rent owed and forbearance for 7%. [3]

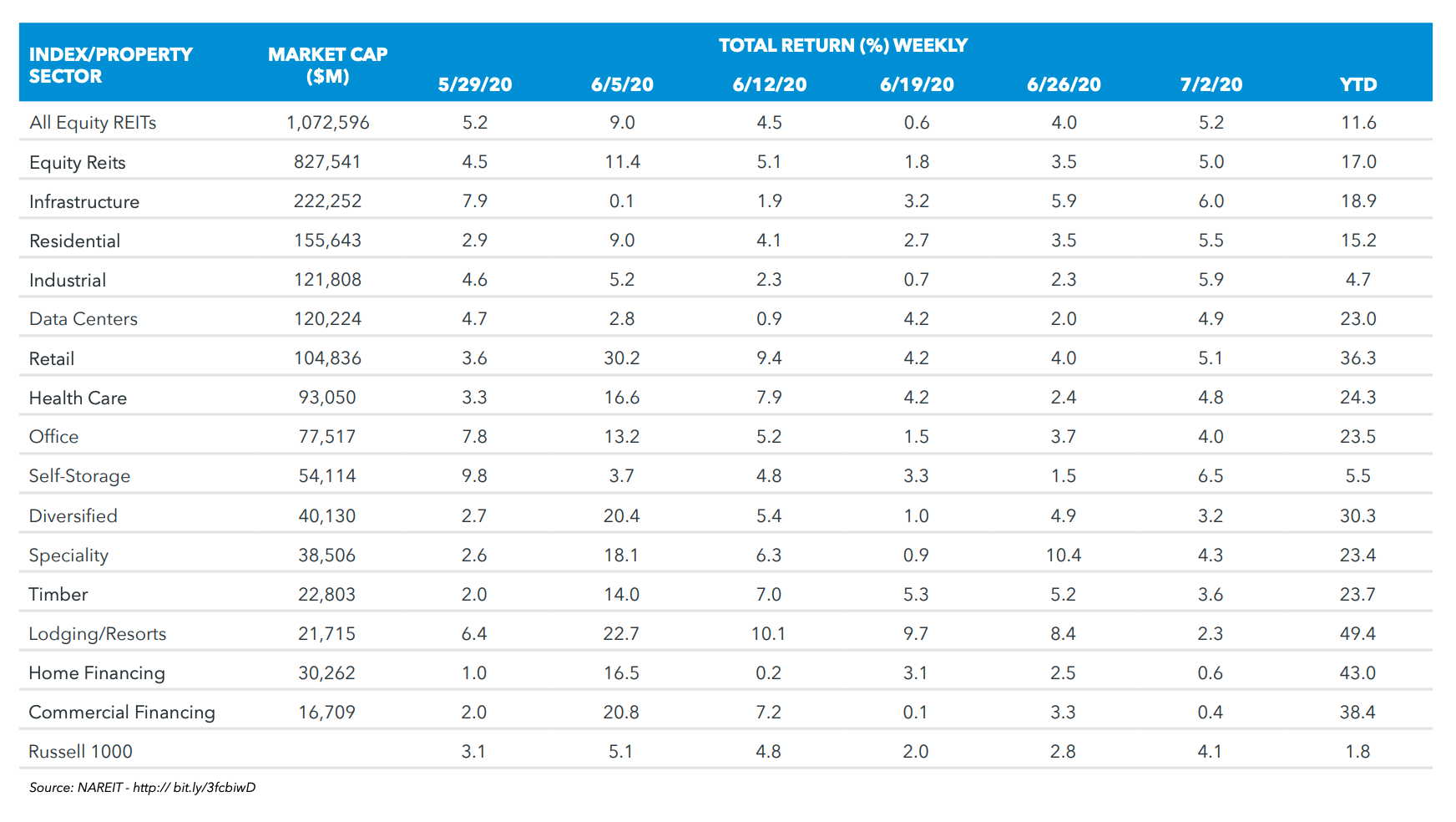

Since the onset of the pandemic, REITs have been increasing the percentage of rents they have been collecting with some sectors approximating 100 percent. This conclusion includes retail REITs, the hardest hit sector. Moreover, REITs have recovered more than three-quarters of the 42% decline from the pre-crisis peak in late February to the trough in late March. As of June 2nd, all property sectors of equity REITs increased. Self-storage led the way with a 6.5% total return, but the infrastructure, industrial, residential, and retail sectors were not far behind. The gains brought total returns of industrial REITs into positive territory for the year-to-date, and pushed this year’s total returns for data centers to 23%. Infrastructure REITs have delivered total returns of 18.9% so far this year. If REITs are any guide to the economy, then they are indicating that the economy, while not out of the woods, is definitely on the road to recovery.

TAKEAWAYS FOR REITS FOR THE REST OF 2020

Notwithstanding the many unknowns ahead—e.g., the potential for setbacks in the fight against COVID-19 as the economy reopens, or the prospect for a vaccine or treatment in the medium-term future—this much can be said with confidence regarding the future prospects for REITs for the rest of the year.

REITs’ strong balance sheets reduce exposures to financial distress and leave them well positioned for future opportunities. Their strong equity capital base reduces pressures to refinance or recapitalize during the crisis. This is in contrast to 2008-2009, when a number of REITs had to raise equity capital at severely depressed prices, diluting existing shareholders. Lower leverage today makes these risks much less likely.

Stronger balance sheets may also allow REITs to take advantage of favorable investment opportunities. In the aftermath of the financial crisis of 2008-2009, many REITs were able to acquire properties at low prices without much competition from other bidders. Many of today’s REITs will be in good position to do so should opportunities arise in the months ahead especially with regard to distressed assets.

REITs will likely experience further cash flow challenges from their operations, and their occupancy rates will likely need time to stabilize. 2019 was an extremely strong year for REITs. It helped he REIT industry begin this crisis from a strong position with record earnings in, high occupancy rates, and strong balance sheets. Most REIT-owned properties are of high quality and their tenants often are financially more secure than those in many privately-owned properties, which may help shield both the tenants and also the REITs themselves from some of the economic damages caused by the pandemic. Barring any unforeseen curveballs, all of these factors should help REITs successfully manage the challenges ahead.