Appraisal Industry: Since Prop 15 mandates assessments every three years, this will create increased-demand for the appraisal industry.

Tenants: Increasing taxes for commercial property owners will lead to higher rents for tenants, which drives up the cost for businesses to operate in California. Small businesses, which employ nearly half of all employees in California, will likely consider out-of-state relocations.

Almost all commercial property leases in all product types contain some kind of clause that requires the tenant to pay all or a portion of property taxes for the space they occupy in addition to base monthly rent. In a net lease, the tenant pays it all from day one. In a typical gross lease, taxes for the “base year” are included in the rental rate with increases for subsequent years passed along to the tenant. But, even in a gross lease the burden is on the tenant because the base rental rate is higher to cover the landlord’s base year levy. As a result, a tenant who occupies a building with a low property tax basis could likely see his or her tax bill double, triple or even quadruple depending on when the landlord acquired the property.

Owner/Users: Because owner/users are both landlord and tenant, it is not possible to avoid a part of the tax increase. In an arms-length transaction, the parties could negotiate who has responsibility for taxes dependent on market conditions. The owner/user cannot.

Typically, owner/users hold a property for much longer than the typical duration of a lease. They do so to fix occupancy cost over the long term by obtaining fixed rate financing and staying in place as long as possible. Generally, those who choose the owner/user route can use the acquired property for 10 years or longer. Thus, imagine the property tax increase for building owners who bought their industrial building for, $50 per square foot back in the mid-1990’s. That property is worth perhaps $270 per square foot today and come 2022, the property would be assessed at current market value and their tax liability would be enormous.

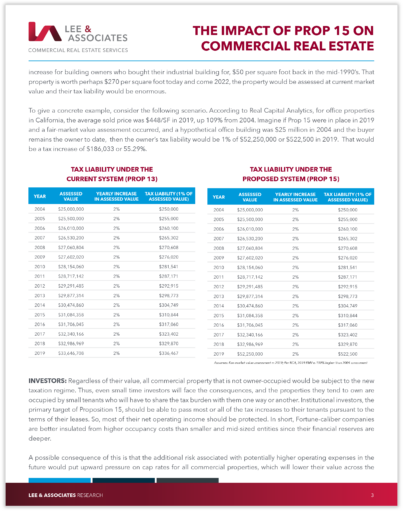

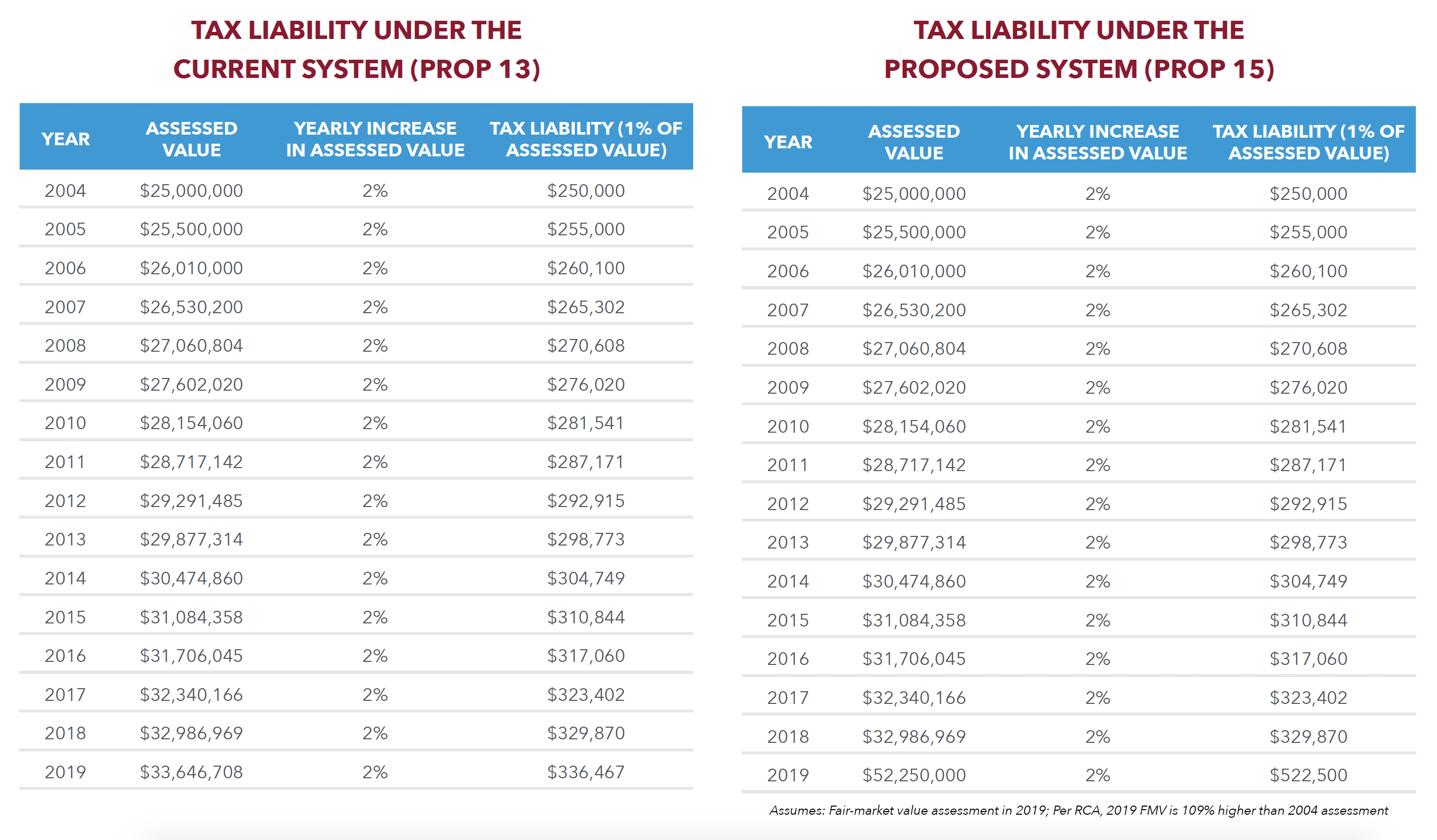

To give a concrete example, consider the following scenario. According to Real Capital Analytics, for office properties in California, the average sold price was $448/SF in 2019, up 109% from 2004. Imagine if Prop 15 were in place in 2019 and a fair-market value assessment occurred, and a hypothetical office building was $25 million in 2004 and the buyer remains the owner to date, then the owner’s tax liability would be 1% of $52,250,000 or $522,500 in 2019. That would be a tax increase of $186,033 or 55.29%.

Investors: Regardless of their value, all commercial property that is not owner-occupied would be subject to the new taxation regime. Thus, even small time investors will face the consequences, and the properties they tend to own are occupied by small tenants who will have to share the tax burden with them one way or another. Institutional investors, the primary target of Proposition 15, should be able to pass most or all of the tax increases to their tenants pursuant to the terms of their leases. So, most of their net operating income should be protected. In short, Fortune-caliber companies are better insulated from higher occupancy costs than smaller and mid-sized entities since their financial reserves are deeper.

A possible consequence of this is that the additional risk associated with potentially higher operating expenses in the future would put upward pressure on cap rates for all commercial properties, which will lower their value across the board. A 1% increase in cap rates (from today’s average of 5%) would wipe out 20% of the current value of commercial properties.

Moreover, for investors weighing multiple state options, such as where to locate a business or where to develop commercial projects, California’s variable tax rates will cause them to think twice before deciding to do business in the Golden State.