Although the pandemic has ravaged many commercial real estate sectors, the industrial market continues to thrive and attract enormous interest from lenders, investors, and REITs. On account of the increase in e-commerce and the continued need for last-mile distribution centers and regional warehouses, asset values of industrial properties are at record highs and the market fundamentals have never been better.

This report will explain the causes behind the industrial market’s success, explain why industrial properties are worthy of investment, and explore the future prospects of this asset class.

E-commerce is now an entrenched fixture of our purchasing ecosystem; there is no end in sight for the demand for industrial assets for the foreseeable future.

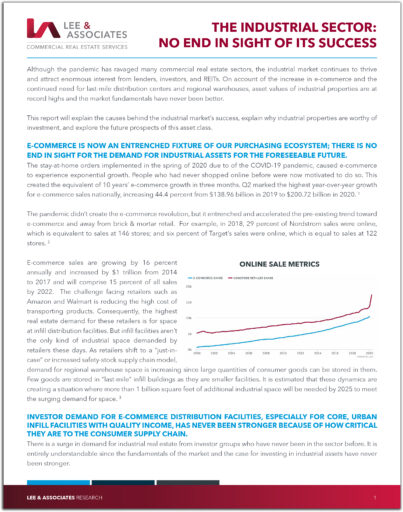

The stay-at-home orders implemented in the spring of 2020 due to of the COVID-19 pandemic, caused e-commerce to experience exponential growth. People who had never shopped online before were now motivated to do so. This created the equivalent of 10 years’ e-commerce growth in three months. Q2 marked the highest year-over-year growth for e-commerce sales nationally, increasing 44.4 percent from $138.96 billion in 2019 to $200.72 billion in 2020. 1

The pandemic didn’t create the e-commerce revolution, but it entrenched and accelerated the pre-existing trend toward e-commerce and away from brick & mortar retail. For example, in 2018, 29 percent of Nordstrom sales were online, which is equivalent to sales at 146 stores; and six percent of Target’s sales were online, which is equal to sales at 122 stores. 2

E-commerce sales are growing by 16 percent annually and increased by $1 trillion from 2014 to 2017 and will comprise 15 percent of all sales by 2022. The challenge facing retailers such as Amazon and Walmart is reducing the high cost of transporting products. Consequently, the highest real estate demand for these retailers is for space at infill distribution facilities. But infill facilities aren’t the only kind of industrial space demanded by retailers these days. As retailers shift to a “just-in-case” or increased safety-stock supply chain model, demand for regional warehouse space is increasing since large quantities of consumer goods can be stored in them. Few goods are stored in “last-mile” infill buildings as they are smaller facilities. It is estimated that these dynamics are creating a situation where more than 1 billion square feet of additional industrial space will be needed by 2025 to meet the surging demand for space. 3

Investor demand for e-commerce distribution facilities, especially for core, urban infill facilities with quality income, has never been stronger because of how critical they are to the consumer supply chain.

There is a surge in demand for industrial real estate from investor groups who have never been in the sector before. It is entirely understandable since the fundamentals of the market and the case for investing in industrial assets have never been stronger.

- Industrial vacancy is at an all-time low. The massive amount of new industrial supply coming to market is being quickly absorbed due to the dramatic increase in online shopping. A large amount of new product has not slowed rent growth. Industrial assets continue to deliver a consistent return on investment (ROI).

- Not only are vacancies low now, industrial properties are expected to have lower, long-term vacancy rates post-pandemic compared to other asset classes. Moreover, longer lease-terms also result in undisrupted cash flow. The top 11 industrial markets are all seeing rising rents, especially in class-A product and product close to urban cores. Expense ratios are typically lower since industrial buildings require simpler construction compared to office or multifamily. This results in fewer and less intense maintenance issues as compared to other asset classes.

- Demand for industrial space has exceeded supply for 42 consecutive months now, with net positive absorption of nearly 57 million square feet in the third quarter, bringing total space absorbed year-to-date to about 120 million square feet. Tight market conditions and solid demand translates into rent growth. As a result, developers remain bullish on the future of the industrial market. Of the 312 million square feet of industrial space under construction at the end of the third quarter, 38 percent is preleased. 4

- Valuations of industrial assets are at record highs and compressing cap rates are at record lows. 5 READ MORE >