- The U.S. industrial market is expected to bounce back stronger than previously forecasted. Annual rent growth will be higher than it was pre-COVID-19, and this increased demand will generate more development going forward. E-commerce companies, food & beverage, consumer packaged goods, and major retailers are highly active, driving the demand for space in markets around the country.[1]

- E-Commerce is stronger than ever. With many brick-and-mortar stores temporarily shut, shoppers have turned to their computers and smartphones to buy everything from fresh groceries to new home furnishings to pet toys. And even after the pandemic subsides, people’s trend of buying more and more online is expected to become long-lasting. The firm eMarketer is predicting U.S. e-commerce sales will make up about 14.5% of total retail sales, or $709.78 billion, this year. By the end of 2024, that percentage will grow to 18.1% of all retail sales, with online sales surpassing $1 trillion for the first time. Consequently, the demand for industrial real estate could reach an additional 1 billion square feet by 2025. To put into perspective how much extra warehouse space that implies, Prologis estimates that e-commerce companies require 1.2 million square feet of distribution space for each $1 billion in sales.[2]

- Prior to the COVID-19 crisis, about 35% of industrial leasing activity was related to e-commerce. Now as much as 50% of industrial leasing activity has been tied to the online retail industry in 2020. As a result, the U.S. is going to need more warehouses to store boxes and handle online orders. As of Q2, the overall vacancy rate for warehouse/distribution space was nearly two percentage points below the cyclical average (2009-2020). Due to the tight market fundamentals, developers have responded in kind and are completing projects even amid COVID-19 challenges.[3]

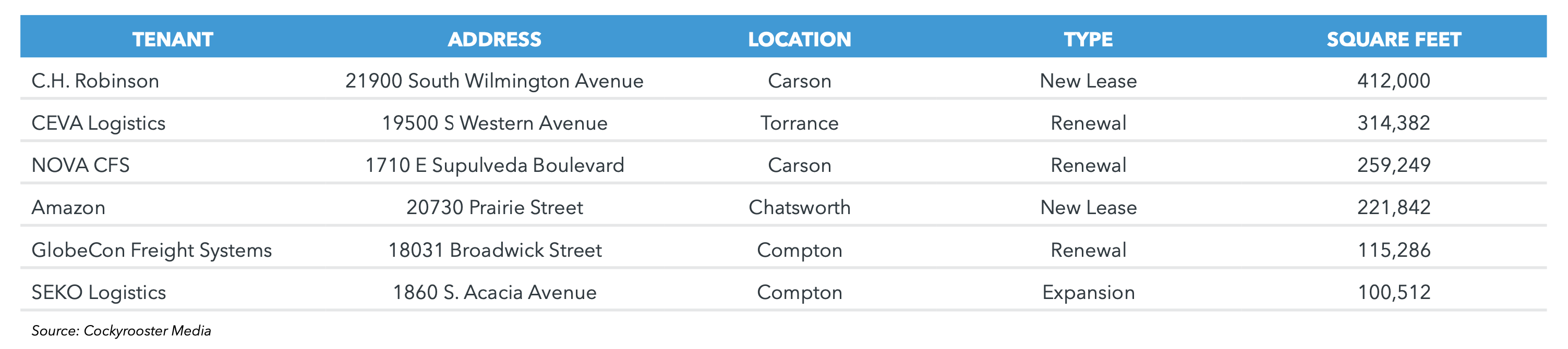

- Bolstering the above points, across all major industrial hubs, the major lease transactions for the past quarter have been e-commerce related firms, i.e., 3PLs and logistics companies. Consider the L.A. Market as a representative example.

- In addition to e-commerce related industries, REIT performance suggests that data centers and infrastructure-related industries have often risen during the COVID-19 crisis, as the use of online communications and cell phone traffic boosts demand for the servers that house the internet and for the cell towers that transmit voice and data communications. Data centers posted a total return of 19.3% by the end of May, while infrastructure was up by 17.9% over the same period.[4]

- Most office occupiers are putting their real estate decisions on hold, as they take a wait-and-see approach since more effects of the economic shutdown and reopening are likely to come to the surface as coronavirus cases surge in the various states.[5]

- To use the L.A. office market as a representative example, compared to the second quarter of 2019, activity was down 65 percent. The economic shutdowns led to the lowest quarter of leasing since the Great Recession.[6]

- Moving forward, the consensus expectation is that the market will continue to shift in tenants’ favor with repricing, and landlord concessions being increasingly generous. But with work-from-home policies relaxing, demand is projected to tick up in the second half of the year.

- Start-ups across the country are letting leases expire and preparing for an extended period of remote work. Start-ups that never intended to be fully distributed are allowing leases to end or looking for ways to get out of longer deals. More prominent employers ar

e closing facilities, consolidating space, and exploring ways to provide workers with flexible arrangements and options closer to home to avoid long commutes.[7]

e closing facilities, consolidating space, and exploring ways to provide workers with flexible arrangements and options closer to home to avoid long commutes.[7] - Credit Karma closed its San Francisco office earlier than expected. It will eventually move all Bay Area employees to its new Oakland office, though some will be able to permanently work from home. Similarly, Facebook, Twitter, Okta, and Box are among the tech companies that have announced a more permanent shift to a hybrid approach. Many others are likely to follow as extended school closures or shortened days make remote options essential.[8]

- With remote work anticipated to become a permanent part of the post-pandemic environment, the emphasis on suburban and secondary office markets increases. This trend predated COVID-19, but the pandemic has only accelerated the trend.[9]

- Office rents per square foot are expected to drop by about 7% from the first quarter to the fourth quarter. Vacancy rates are expected to rise 14.9% in first quarter of 2021, up from the 12.3% in the first three months of 2020.[10]

- Compared to July 2019, job postings—a real-time measure of labor market activity—are 23.3% lower as of July 10, 2020. Keep in mind that the economy has only slowly started to reopen, and thus the 23.3% decline is a positive sign since it is an improvement from the 39.3% year-over-year decline witnessed in May of this year.[11]

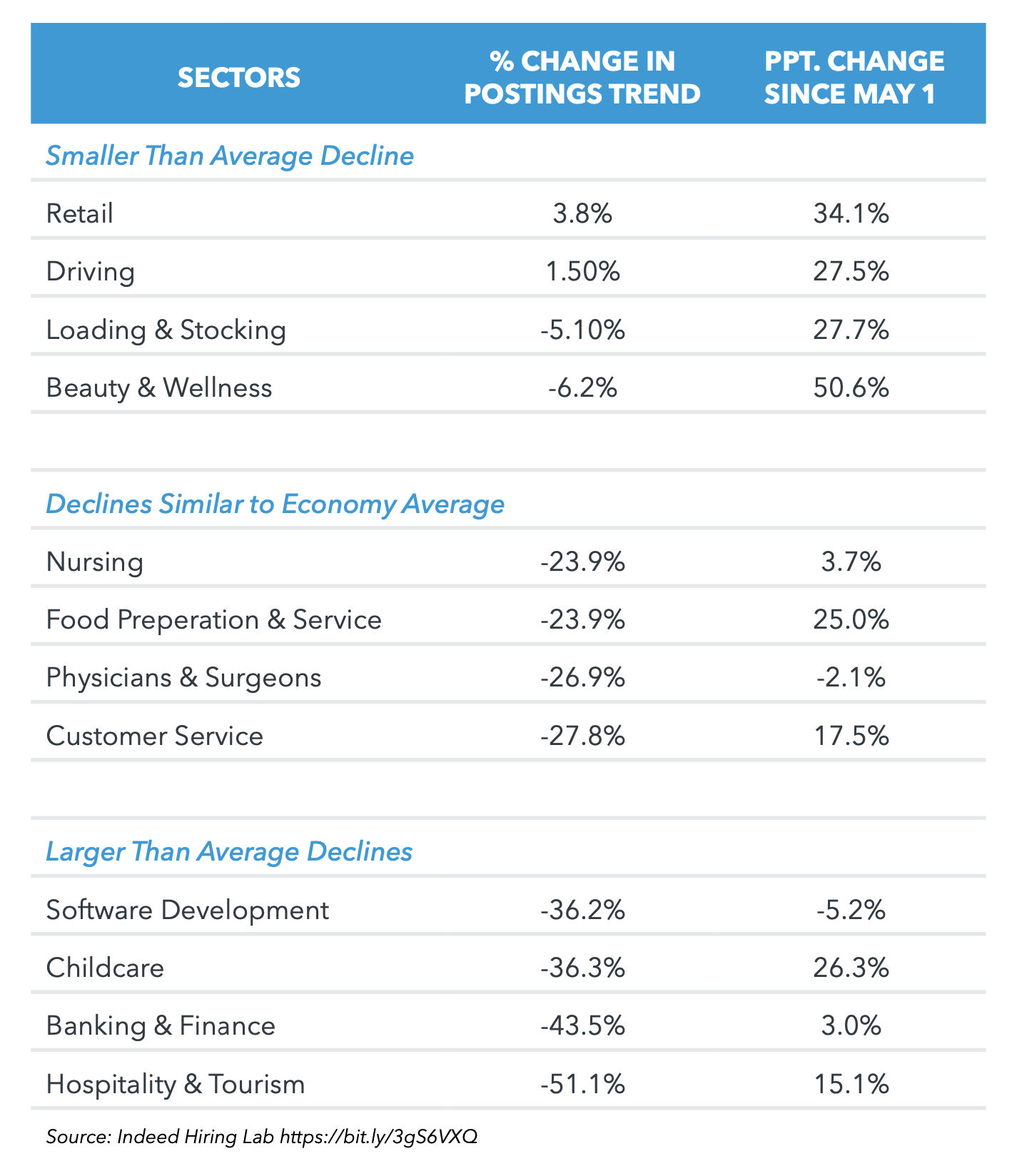

- In terms of employment availability, the hardest-hit industry sectors are as follows in chart 2.